Juniper CEO: The bet we made on the enterprise is really starting to work

Dec 29, 2022

You can often gauge the ambition of a tech company based on the size of the problem that the company tackles. Think of Amazon, which early in its existence shifted from the already gigantic goal of being the world’s biggest bookseller online to the even more gargantuan aim of being the biggest seller online of anything and everything.

Juniper Networks started out twenty-six years ago with the audacious goal of giving serious competition to Cisco Systems, the incumbent vendor of networking equipment to phone companies. What was essential was the scale of the problem. Founder and then-CTO Pradeep Sindhu explained to me at the time that Juniper was seeking to solve the utter havoc that the Internet had brought to phone company networks, something Cisco hadn’t adequately addressed, leaving a hole to fill.

Sindhu even had a vivid technical term for the problem, “the small-packet tsunami.”

Don’t worry if you don’t know what a small-packet tsunami is, or even what a packet is. All you need to know is that solving the small-packet tsunami for phone companies succeeded superbly, and Juniper became a very viable and very prosperous second choice to Cisco. That lead to huge revenue growth for many years.

Somewhere along the way, Juniper sought a second act as revenue growth cooled. For a time, the shift to cloud computing was the biggest challenge facing the networking world. While Juniper did well selling to cloud computing operators, its sales growth still languished.

Suddenly this year, sales growth is sharply higher at Juniper, higher than expected, and Juniper shares are outperforming those of peers and of the broader market. It seems the company may have found a problem of size and scope worthy of its ambition.

“One of the biggest bets that I made when I took the CEO role was on the enterprise,” says Rami Rahim, who just completed his eighth year running the company, in an interview he and I had earlier this month via Microsoft Teams.

“There were quite a few skeptics, both inside and outside the company,” says Rahim, “but we nonetheless charged forward.”

“That bet we have made on the enterprise is really starting to work,” he says.

The term “enterprise,” in this case, means selling Juniper equipment to the largest corporations in the world to run their own internal networks, and it means eating into Cisco’s most valuable franchise.

STORMING THE ENTERPRISE

From almost nothing a few years ago, Juniper’s equipment has risen to 2.4% of total industry revenue for “campus” switching equipment versus Cisco’s 56.4% in the third quarter of this year, according to Mauricio Sanchez, Research Director with market research firm The Dello’Oro Group. Juniper has also taken meaningful share in other categories, says Sanchez, including 4.3% of data center switching, versus 28.6% for Cisco.

“We are a relatively small player,” concedes Rahim. A number of other vendors compete, including Arista Networks, China’s Huawei, and Hewlett Packard Enterprise. And some of them have larger share than Juniper.

But that may not matter as much as the fact that the prize is big. Enterprise is a twenty-billion-dollar market annually, says Rahim, and more if one folds in a lot of additional categories of enterprise networking beyond the campus switches and data center.

“It is a massive market, we have very small share, and we enjoy significant market differentiation, so that's a great recipe for continued sustainable growth.”

The contribution to growth is impressive. From nearly seven percent revenue growth last year, Juniper’s sales this year are expected to rise by twelve to thirteen percent, the company projects, higher than an expectation earlier this year for just ten percent. The outlook for next year’s revenue growth of “at least seven percent” is also higher than initially expected.

In the September quarter, Juniper’s sales rose by nineteen percent. Sales to enterprises, at $516 million, was neck and neck with the company’s sales to service providers, and both rose about seventeen percent. But, “I expect the enterprise will be our fastest-growing segment” going forward, he says.

“For the first time in history, in Q1 of this year,” the March quarter, “we reported an enterprise quarter that was actually bigger than service provider and cloud” revenue, notes Rahim.

“Within a few years, enterprise will not only be the biggest segment, it will be the majority of Juniper's revenue,” he says.

COMPLEXITY IS IT

The enterprise opportunity, like the opportunity a quarter century ago, at Juniper’s founding, is an opportunity to tackle vast complications inside companies’ networks. It is a degree of complexity not seen before, wrought by the simultaneous occurrence of several new factors: the continued movement of everything to cloud computing; the "new world of work” and its sudden requirement that everyone be working a little bit remote, a little bit in an office, and a little bit on the beach; the rise of numerous unauthorized “Internet of Things” devices connecting to networks — and on and on and on.

“My problem right now is battling complexity,” says Rahim of the new regime. “I have so much of my team just keeping the lights on, working day in and day out with the proverbial pager attached to their belts, getting calls in the middle of the night because the experience to my end user is terrible.”

Add in, of course, the fact that the pervasiveness of networking since the pandemic lockdowns makes all of it more serious as employees and customers and shareholders and suppliers all expect everything to be delivered to their devices.

“Enterprises today are dealing with massive complexity challenges, and if you can give them a simple solution that actually just works and works effectively for the applications that they care deeply about, you win,” says Rahim.

Rahim is the kind of individual you would want running a complex technology business. Employee number thirty-two at Juniper at its start, he has a deep attachment to the the technology, the products — the most successful of which he helped build — and by now, an extensive sense of what works and doesn’t work.

OUT OF THE MIST

Juniper’s success in selling to the enterprise so far is thanks in no small part to an acquisition Rahim had Juniper make back in 2019 of a startup called Mist Systems, nestled in Cupertino, not far from Juniper’s Sunnyvale, California offices in Silicon Valley. Mist had patented technology to automatically detect what’s going on with a piece of networking equipment, such as when a laptop user has a problem connecting to the WiFi access point.

More important than just detecting, the company had developed ways of sorting and sifting such data to divine where there are patterns of problems. Using machine learning forms of artificial intelligence, including what are called “recurrent neural networks,” the Mist software would correlate events that happen in time. Something as simple as a WiFi access point rebooting itself, or multiple frustrated users unable to get a signal were clues. The Mist software would chase down a root cause, such as a software upgrade that had introduced errors into the functioning of the equipment.

This kind of stuff is known as “AI Ops,” meaning, using artificial intelligence to automatically do some of the things that IT people would do manually to keep things running.

IS AI FOR REAL?

When it comes to AI, as a reporter covering AI for a long time, I automatically flinch. I’m inclined to be skeptical that anything AI does what the sales pitch says.

“There are a lot of AI skeptics out there, and I understand, because I am a recovering skeptic,” says Rahim. “There’s a lot of skepticism because there's a lot of AI washing out there,” which is certainly true, especially in industry.

“But, I think that, actually, AI is truly revolutionary, and the impact is totally underestimated by most people,” says Rahim.

What I have not yet grasped, says Rahim, is that there is what you would call a feedback loop. The AI program or programs process more and more data, in this case, signals from the network about how everything’s doing, and the programs gets better at detecting the flaw the signals are collectively shouting about.

The idea is akin to Metcalfe’s Law, which is not a law, but a kind of heuristic, named for Ethernet networking inventor Bob Metcalfe, which says that the value of a network increases as more and more people participate in it.

“There’s a similar sort of effect, one not yet named,” says Rahim, comparing AI to Metcalfe’s Law.

“If you could accumulate data and then you can leverage that data to become smarter about a particular problem you're trying to solve — and, obviously, you can't do that through human processing, it's just way too much data, you need to have artificial intelligence — then what you do is you leverage that knowledge and that insight to improve the service or the product or the solution that you're delivering to your customer.”

The Mist software runs in a cloud computing facility, so it sees everything from all its customers. The eyes on everything start to amass a shared history of collective patterns of behavior. Mist represents “an AI engine that has been learning over the last six years or so about what is good and what is not good,” as Rahim puts it.

“What ends up happening is your customers are delighted” as the software fixes things like the inability to connect to the WiFi, he says. “And they buy more and you acquire more customers, and guess what happens when you do that, you accumulate even more data.

We are winning very large enterprise franchise deals today,” says Rahim. “And it's not like we're getting table scraps or, you know, a small percentage of share to keep the primary vendors honest — these are big, new, wonderful opportunities.”

“And that additional data gives you even greater insight, which improves the product even more, which results in this virtuous flywheel effect that's extremely powerful.”

Rahim liked the Mist AI so much, he had Juniper spread it beyond just the WiFi access points, to more and more of the networking boxes Juniper sells.

A PROBLEM OF SCALE

The question, of course, is why this is a problem of size and scope worthy of Juniper’s ambition. Says Rahim, everything gets more complicated when trying to use Mist to serve the biggest companies.

“We have one customer that has north of one hundred and fifty thousand Juniper network elements,” he says, where every “network element” is a networking box with lots of cables and lights and switches connecting stuff. “Every one of those network elements is providing us insight about the end user experience every one or two seconds.”

Networking, at its most basic, is “a game of scale,” a realm in which “it’s easy to do something for one to a dozen users,” but, “it’s a whole different ballgame to be able to do it for millions and millions of people that are using the network for whatever purpose.

“It's so important to be able to do this at scale, for every user that's on the network, around the globe,” says Rahim. “And, yes, it's as hard as it sounds.

“That is precisely the problem that we have solved.”

The payoff for a customer is reduced labor for the IT staff, and faster everything, says Rahim. “A total reduction in trouble tickets, ninety-plus percent, and a massive reduction in resolution time” are things customers are seeing, he tells me. “What used to be many months to deploy a new network, we can do it in a few weeks.”

The small startup that was Mist, notes Rahim, inside of Juniper has grown to represent $850 million in annualized sales at the current “run rate.”

“It’s been a big home run for us.”

STOCK BOOST

As Mist has pushed Juniper’s enterprise foray into forward momentum, it has had a noticeable impact this year on Juniper stock. At a recent price of $31.36, the shares are down just twelve percent this year, way better than the twenty-five percent drop of Cisco, and the seventeen percent decline of Arista, and, obviously, way better than the thirty-four percent dive in the Nasdaq Composite Index this year.

The outperformance is surprising given that in Rahim’s eight years at the helm, Juniper stock’s total return on an annualized basis is 6.8%, trailing Arista’s, 28%, and Cisco’s, 10%.

How far, I wonder, can Juniper go in taking share from Cisco, and from others such as Hewlett Packard? It is not hard for a company to bite off a bit here or there, to be a convenient alternate supplier to customers. But to take successive billions of dollars, year after year, is something else.

“We are winning very large enterprise franchise deals today,” says Rahim. “And it's not like we're getting table scraps or, you know, a small percentage of share to keep the primary vendors honest — these are big, new, wonderful opportunities.”

It has taken many years, says Rahim, to build teams to sell the products into enterprise, where Cisco’s dual powers of its massive direct sales force, and its relationships with resellers and systems integrators, have always reinforced customer loyalty.

“That was all new muscle that we built over the years,” he says of redeploying sales and marketing, “and the go-to-market team has really executed exceptionally well on that front.”

The playbook for this move into Cisco turf is very much the one that worked in the early days going up against Cisco, says Rahim: prove yourself, and then build from there.

“Sometimes there are these very large RFPs, and you become an incumbent in a very large network” for a very large customer, he says. But not always.

“There are other occasions where the strategy is one of a small insertion, leveraging that small insertion to demonstrate that you can be a very viable, larger, more strategic partner to a customer and then expanding from there.”

“You have to go in and say, Look, just deploy me in this one little area, and then, if you like us, give us more business.”

JOUSTING WITH ARISTA

Arista, of course, is also pushing into the enterprise, as I discussed with Arista’s CEO Jayshree Ullalearlier this year. Rahim says Juniper rarely goes up against Arista in the campus switch category of enterprise. In that category, Arista has only about 1.1% share, according to Dell’Oro’s Sanchez.

In the data center, where Arista has 21.1%, closer to Cisco and well ahead of Juniper, Arista is a factor, he said.

“They're certainly going after that market opportunity, and I understand why, it’s a large and lucrative market opportunity,” says Rahim. "But I would say that this is where we are taking share faster than anybody else.”

The data center market will get even more interesting in 2023 and beyond as enterprises move closer to adopting the fastest networking speeds in their facilities, moving data at fiber-optic speeds of four hundred billion bits per second, known as “400G,” or “400-gig.” Those kinds of big upgrades come every few years, and when they do, they are a boon to equipment vendors to sell a new wave of equipment, like an iPhone with a much better camera.

“400-gig is an extremely important market opportunity for us,” says Rahim. “It’s happening today in the service provider and cloud market; it’s not yet a big trend in the enterprise but it will come, and it will play out over a few years.”

RE-SHAPING THE COMPANY

If the immediate payoff has been a boost to Junipers’ sales, what is the longer-term achievement for the company? As Juniper goes up against Cisco and others, will they merely make a dent, or will the company be actually changed in some way?

That sales muscle to which he refers, says Rahim, the ability to first win a seat at the table, and then learn to nurture large enterprise accounts, will leave its mark on Juniper.

“Once you've inserted, it’s a muscle of cross-sell and up-sell of new capabilities,” he says. “That is going to achieve a larger Juniper, a more profitable Juniper, a more resilient Juniper.”

The ability to meet or exceed expectations has been commendable since Rahim and CFO Ken Miller laid out a plan for the Street at the last analyst day event, in February of 2021. At the time, Miller said Juniper would see revenue growth of three to four percent in 2021 and “at least low single-digit” growth in 2022 and 2023. The company has now blown past those promises with the results this year, and with the higher-than-expected forecast for next year.

“We have exceeded all of our three-year plan,” says Rahim. In addition to revenue growth, Miller promised non-GAAP operating profit margin will “expand each year,” via a combination of keeping expense growth slower than revenue growth, and boosting gross profit by selling more and more software such as the Mist AI programs. Software automatically comes with higher profit margin than machines made of sheet metal.

The profit picture this year looks good. From a non-GAAP operating profit margin of 15.9% in 2021, taking into account the company’s forecast for the current quarter, Juniper is on track to make a profit of a little over eight hundred million dollars on revenue of $5.3 billion this year, a margin of eighteen percent.

LOOK PAST THE SUPPLY CHAIN

As good as these numbers look, it is rather striking that Juniper has managed those results given the continued deleterious effects of the supply chain. Like Arista and Cisco and others who ship physical product, Juniper has been going to extraordinary measures to get its supply of chips, and to wrangle special freight arrangements here and there.

“I actually get quite involved in working directly with our strategic suppliers to get our fair share of components,” says Rahim. “We're shipping meaningfully more product this year than last year, but is it normal? No. Are we still sitting on massive backlog that we're trying to work through? Absolutely.”

Things will continue to improve through next year, “but it will still not be normal.”

Rahim directs investors to think about the potential upside as supply issues eventually abate. “If in fact the supply situation next year becomes materially better, then I think we should be able to exceed that at least seven percent [revenue growth forecast] meaningfully,” he says.

Profit, too, can get a lift. Juniper this year paid $155 million more than usual for expedite fees and broker costs on additional freight arrangements. “Next year, I don't think the full $155 million in incremental cost of supply goes away, but I do think it gets better,” he says. “So, that bodes well for building more leverage in our P&L, essentially seeing that that revenue growth translate to operating margin expansion.”

CAPITAL RETURNS

Expansion of operating profit is an immediate proxy for capital returns to shareholders, as the company has pledged to pay out half its free cash flow, annually, in the form of dividends and buybacks. Juniper has frequently exceeded that, including this year, even as unprecedented capital costs for supplies weighed on its cash flow.

The company’s been active most quarters in buying back a couple of percent of its shares outstanding, and the dividend has steadily increased since Rahim has been CEO. The current payout, twenty-one cents per share per quarter, is a healthy 2.7% yield.

With success this year and last, and probably in 2023, it seems time for another analyst day, I offer. “Stay tuned,” he says. “I know our investors certainly have been asking about it, so we will schedule one shortly.”

As we conclude our chat, I have the chance to ask one of my favorite questions for CEOs and CFOs. At the current price, Juniper trades for two times next year’s projected revenue, as a multiple of enterprise value divided by sales.

Is that a good buy? I ask.

“Look, I can't say whether it's a good buy or not,” Rahim replies. “What I can say is the following: I am a huge believer in our ability to continue to be successful in winning in the market, and in using that to grow our financials, our revenue and our operating margin, in the future. And I think that's going to bode well for our stock price.”

Investors warm to software just a little bit

Dec 27, 2022

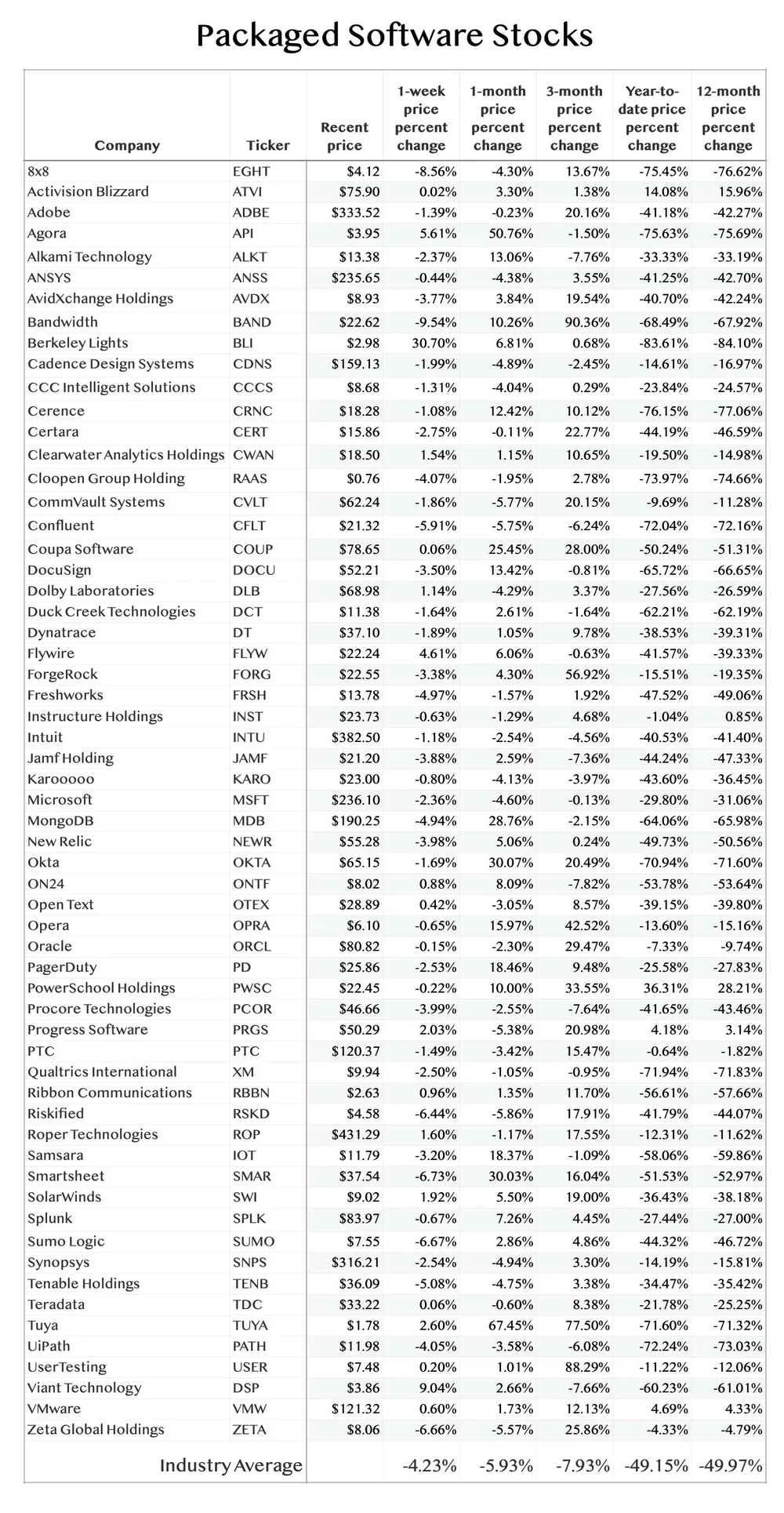

Some software stocks have had returns in the one- and three-month periods that defy the gloomy state of the software market.

Most of this year, software stocks have been among the bigger disappointments. Out of about five hundred tech stocks I regularly follow, most but not all of which are U.S. firms, the average price decline for the industry designated “packaged software” is just under fifty percent this year.

Out of forty-seven industry categories in the five hundred or so stocks, that sharp drop puts packaged software in the bottom twenty of industries. Semiconductors are down only thirty-seven percent in that time, by comparison, and the group of electronic components names, including Corning, has been among the strongest, down only fifteen percent.

The poor performance is not surprising given massive disappointments in the most recent earnings reports from names such as Twilio and Crowdstrike. Software sales have been under pressure for pretty much every vendor, whether they have met expectations or not.

However, in the past month to three months, software performance has brightened. The average decline for the packaged software group in the past month is just under six percent, better than the one-month average across all industries of an eight percent decline.

And while software trails on a three-month basis, down almost eight percent versus an average of all industries of down three percent, some software stocks have notched extraordinary gains in those three months, such as Nutanix, up twenty-two percent in three months.

Below is a list of the sixty software names among this group that have beaten the average for one-month and three-month returns.

Software names that have done better than average on a one-month and a three-month basis.

Why is this happening? It’s not tied to quarterly financial outperformance or underperformance. For example, GitLab, a company that has delivered results that defy the gloom in software, has had a weaker-than-average three months, down twelve percent.

But Dynatrace, which had to cut its outlook last month, nevertheless is up almost ten percent in three months, and has managed to be just a little better than flat the past month in comparison to that nearly six percent average decline.

Rather than hypothesize some over-arching theorem, I would suggest there are a variety of things going on. I think the “expectations reset,” as they say on the Street, where bad news is baked in, allows some buyers to creep back into a stock such as Dynatrace.

Dare I say it, some software investors may feel they’re getting bargains in some beat-down names. Confluent, for example, is a company that is not profitable, and won’t be for years yet. (Street consensus is that it loses money through 2024, and there’s no consensus yet about 2025.)

But Confluent has had better-than-average performance in three- and one-month periods. Its results have held up better than some other names, and after a seventy-two percent decline this year, Confluent trades for a multiple of enterprise value to next twelve months’ revenue of six and a half times. That is lower than the multiple of eight times just six months ago, and way below where Confluent traded at a year ago: thirty-four times revenue.

Perhaps that doesn’t sound like a screaming buy to you, but I can imagine that some folks must be eyeing the multiple contraction for stocks such as Confluent and thinking that if the estimates are correct, then the stocks are a decent buy relative to the exorbitance they once commanded.

The TL podcast for December 26th, 2022: Azenta is tops, pondering Absci, another awful Tesla week

Dec 27, 2022

Chip stocks continue to lose altitude but investors liked Azanta (AZTA), Tesla (TSLA) was once again a mighty dog, life sciences AI hopeful Absci, and predictions of AI doom from one of AI’s luminaries.

Solar bubble? Enphase retains pricey valuation

Dec 23, 2022

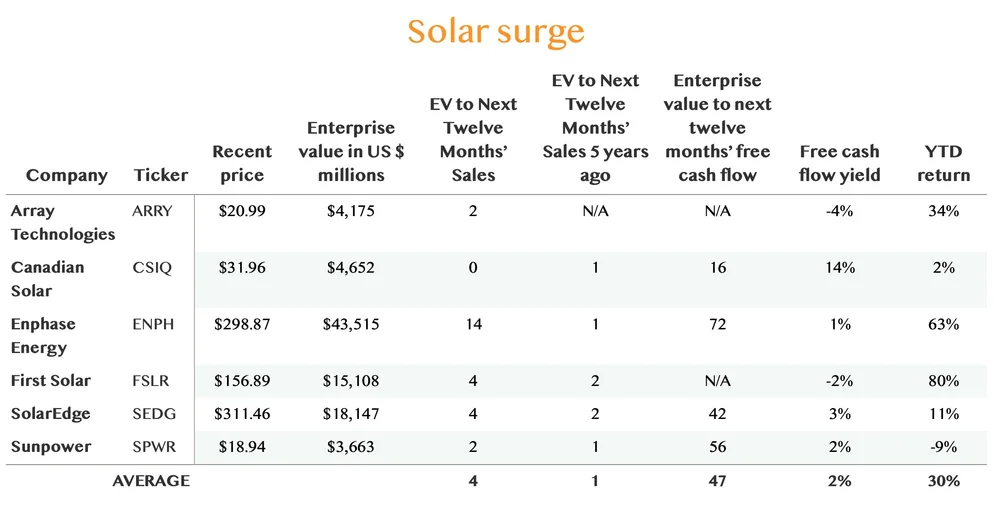

It’s not news that this year’s multiple energy crises, including the soaring price of gasoline in the first half of the year, and now the prospect of Europe starved for oil during the winter because of Russia’s war in Ukraine, have been a boon to the solar energy industry.

These are a gaggle of hardware vendors that include the bellwethers, First Solar and Sunpower, two panel makers that have been around since the previous solar boom, in 2007 or so; and some newcomers, including Enphase and Array Technologies, the former a maker of “inverters,” the latter a maker of “trackers” for solar farms.

As you can see in the accompanying table, the stocks of the group are up an average of thirty percent this year, pretty terrific. As interesting, their average stock valuation as a multiple of enterprise value divided by the next twelve month’s sales, has risen from one times a year ago to four of late.

One stock in particular stands out as having special momentum, if you will. Enphase, which came public back in 2012, has the second-highest revenue growth rate after Array, and unlike Array, it is profitable, with expectations it will make about $606 million in free cash flow over the next four quarters, according to FactSet estimates.

And Enphase has a perfect four-year record of topping analysts’ sales expectations, versus the rest of the group, which have done rather mixed in their reporting. I first pointed this out last year, when I wrote that Enphase was managing its business very well considering that it was struggling during the supply-chain mess to get parts to build its inverters.

Enphase builds what are called “microinverters,” parts that convert energy from DC to AC power in a solar energy system, and that do it in a “distributed” fashion, which has advantages over traditional inverters that are “centralized.”

Enphase has been riding the wave of home solar installation with the inverter product, and with a contractor model that lets a third party install the devices on the roof. Sales are expected to rise sixty-seven percent this year, to $2.3 billion. To be that size and growing that fast is impressive.

What strikes me in particular is the valuation. The company trades for a whopping fourteen times the next twelve months’ projected revenue. That kind of sales valuation makes it one of the most expensive stocks among the five hundred or so tech names I regularly follow.

In fact, in my collection, Enphase has the same multiple of enterprise value to sales as Snowflake, the cloud database software vendor. On some level, that kind of multiple makes sense because they are of similar scale and growing at similar rates.

Enphase is a little cheaper than Snowflake on a profit basis, at seventy-two times projected free cash flow versus ninety times for Snowflake. And its free cash flow yield, meaning, its free cash flow divided by stock price, is better, at 1.5% versus 1.10% for Snowflake.

That looks like a good deal, given that Enphase is doing better at generating real cash profits than Snowflake. Although Enphase has a lower gross profit margin, at forty-one percent versus Snowflake’s seventy percent, Enphase has a free cash flow margin of twenty percent, twice that of Snowflake.

And yet, it is rather extraordinary for a hardware maker such as Enphase to trade at the same or similar multiples of sales and earnings as a software maker. Typically, there’s a discount for the lower gross profit margin, and the greater risk, of a hardware maker. That greater risk is in contrast to cloud software sales, where there is a degree of certainty baked into the way software is billed and invoiced.

I’m inclined to think that the sixty-three percent run-up in Enphase this year is an effect of traders fixated on the energy crisis story, and that the stock has gotten ahead of itself.

But maybe uniqueness plays a role. Over the transom Thursday came a long report by Daiwa Capital Markets analyst Jonathan Kees, in which Kees initiates coverage of Enphase and First Solar with “Outperform” ratings, and a Neutral rating on SolarEdge.

Kees believes the outperformance of the group can continue, and Enphase and First Solar, in particular.

With respect to Enphase, Kees’s three principle points are that a) there is, indeed, an energy crisis, maybe temporarily with the Ukraine war but permanent given broader risk; b) Enphase is in a duopoly with SolarEdge for inverter sales in the U.S., and duopolies tend to be a favorable structure for protecting pricing; and c) the Inflation Reduction Act passed by the U.S. Congress is a windfall for further building.

Kees notes that the stocks have all become something of a momentum investment. “In our view, the sector has gone from high-risk and somewhat distressed to high growth and momentum,” he writes. “We believe the run over the last three years can continue even with higher interest rates as utility companies to homeowners can justify the higher cost of capital by raising rates or saving more money on utility bills.”

On the matter of energy security, it’s top of mind everywhere, he writes: “Geopolitical events like the Ukraine war have highlighted the vulnerability of energy security. The lack of global investment in fossil fuel development also can keep supply/demand tight and prices high, barring a recession.”

On the matter of duopoly, Kees writes that Enphase and SolarEdge have about ninety percent of the U.S. residential market for inverters. That’s thanks in part to the fact that the world’s dominant seller of inverters, China’s Huawei, is banned from selling in the U.S.

Enphase, writes Kees, has been doing better than SolarEdge within that duopoly: "Enphase has gained market share over SEDG in the US residential market. This favorable market has high growth and high margins.”

On the matter of the Inflation Reduction Act, it’s one of several initiatives he thinks will add fuel to the fire, so to speak: “We believe the sector is now entering a catalyst-rich environment as companies announce new manufacturing facilities to benefit from the US Inflation Reduction Act (IRA), and for order activity to accelerate during 2H23 owing to that policy, providing booking visibility into 2024-25.”

As far as valuation, Kees thinks the multiples on the entire group are “surprisingly reasonable” given how much the companies have to offer. His main defense of the stock multiples is that the stocks are “within historical range.” Meaning, Enphase’s historical multiple of sales over a two-year period is 13.3 times, not far from what it is now.

I suppose that’s true, though it ignores the fact the stock has been much cheaper many years ago. I still suspect some of the valuation is that momentum trade from a market that is enamored of alternative energy as a narrative at the moment.

I also suspect that some of the hot air that came out of Snowflake and other pricey software stocks went into these renewable energy stocks, especially Enphase.

Probably, as Kees suggests, as long as the results at Enphase continue to deliver, it will maintain the momentum, and that keeps the stock high.

As for the title of this article, it may not really be fair to call it a bubble, for one stock does not a bubble make. However, I suspect that regardless of individual valuation multiples, there is a bit of the momentum element in all of th names, as Kees suggests.

Micron: the auto market for chips is soaring

Dec 21, 2022

Update:

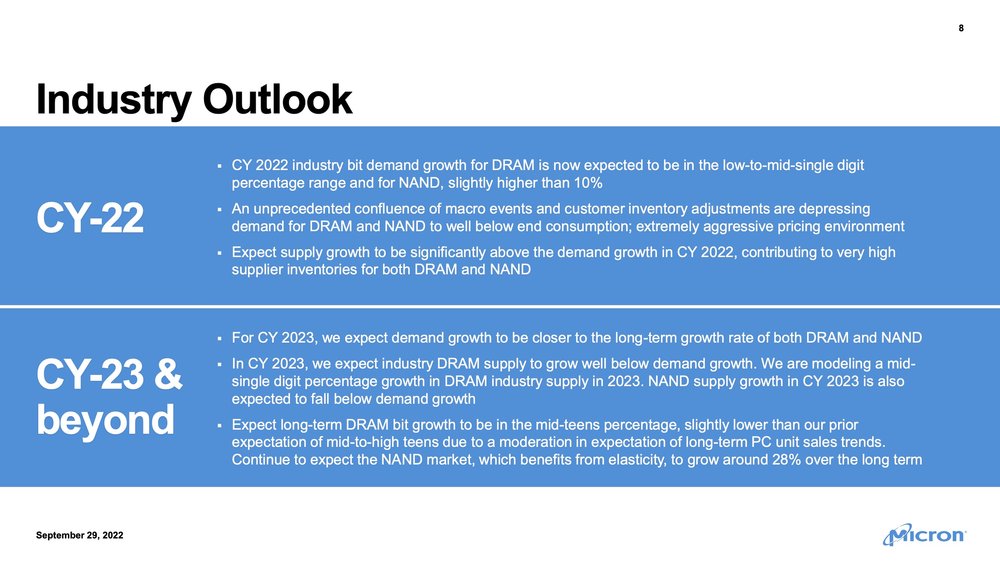

On the call this evening, Micron CEO Mehrotra told the analysts the company is navigating “the most severe imbalance between supply and demand in both DRAM and NAND in the last 13 years” and that pricing for chips, industry-wide, “deteriorated significantly” since the last earnings report.

Although the glut of chips sitting in inventory with customers is going to burn down to “healthy” levels by the middle of 2023, said Mehrotra, which will boost Micron’s revenue growth, he predicted that profitability in the DRAM and NAND business will “remain challenged” all year long for all industry participants.

On the positive side of things, Mehrotra gave analysts a taste of how some markets for chips may see improvement:

Automotive: Sounds the healthiest. Micron’s revenue for chips for cars was up thirty percent last quarter, almost as good as the record quarter prior to that. “The macro environment does create some uncertainty for the auto market, but we see robust growth in auto memory demand in fiscal 2023,” said Mehrotra. The growth in the demand for memory chips, by volume of bits, will be double that of any other end market for the next five years, predicted Mehrotra.

Flash-based solid-state drives: Had a "very strong” quarter, and Micron has leading technology for “QLC,” the highest-density form of NAND flash that allows for replacement of disk drives. This sounds like what Charlie Giancarlo, CEO ofPure Storage, has been saying about replacing disk.

Smartphones: After sharp declines in handset sales this year, things are going to rebound from China’s unlocking, says Mehrotra. “We forecast calendar 2023 smartphone unit volume to be flattish to slightly up year-on-year, driven by improvements in China following the reopening of its economy.”

Industrial: IoT and 5G base stations and other infrastructure are still good markets but are soft at the moment; they should rebound in the second half of 2023, said Mehrotra.

On the negative side, the biggest concern is not the glut of chips itself, it’s what it’s doing to prices of chips for Micron and others. Prices of chips declined by more than 20% for both DRAM and NAND last quarter.

Hans Mosesmann of Rosenblatt Securities, in a note to clients this evening, points out the pricing issue is going to last for about six months.

Mosesmann writes that “indications are that we are bottoming in terms of industry and company inventories.” But, writes Mosesmann, that just means that “we exit in the first half of calendar ‘23 the inventory “bit” problem and enter into a headwind centered around ASPs, which we see stabilizing entering second-half calendar ’23."

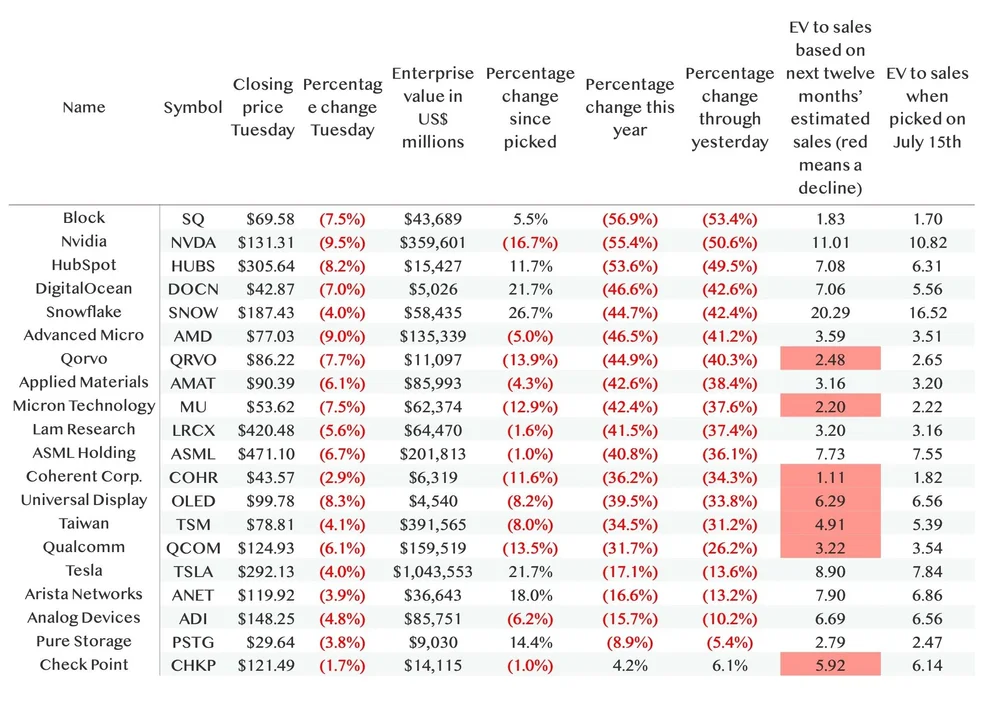

With tonight’s slide in the stock to $50.26, Micron shares are down eighteen percent since picked for the inaugural TL20list of stocks to consider.

Previously:

Shares of memory-chip powerhouse Micron Technology declined by one percent in late trading after the company this afternoon reported fiscal first quarter revenue and profit that missed analysts’ expectations, the third time in a row it has missed sales expectations and the first time in quite a while the company has missed profit expectations.

CEO Sanjay Mehrotra noted the company met its own forecast “despite challenging conditions during the quarter,” and said the company is on “solid footing to navigate the near-term environment,” adding, “we are taking decisive actions to cut our supply and expenses.”

Mehrotra continued, “We expect improving customer inventories to enable higher revenue in the fiscal second half, and to deliver strong profitability once we get past this downturn.”

The company’s forecast for revenue and profit this quarter was also disappointing, the third quarter in a row of weaker-than-expected forecasting.

In a companion deck of slides, Micron said it sees NAND flash memory chip sales coming in lighter than previously expected this year, changing its language for “industry bit demand growth” for NAND from “slightly higher than 10%” in its previous report to now “low to mid-single digit percentage range.” That’s not a big surprise for anyone watching the collapse of NAND pricing this year.

For 2023, the company thinks demand for DRAM will rise by ten percent, and for NAND, by 20% or so.

That is a moderation from the prior quarter’s statement, “For CY 2023, we expect demand growth to be closer to the long-term growth rate of both DRAM and NAND.”

Micron again cut its outlook for its capital spending, to a range of seven billion dollars to seven and a half billion this fiscal year, down from an already reduced eight billion in the prior report.

It said its spending on wafer fab equipment, or “WFE,” will decline this fiscal year by “more than 50% Y/Y,” which is sharper than the prior language, “nearly 50% Y/Y.”

The company said its own supply in DRAM is going down this fiscal year:

Expect Micron’s CY23 production bit growth to be negative in DRAM and up slightly in NAND. Full impact of the wafer start cuts will be realized beginning FQ3-23. Micron’s bit supply in 2024 will be materially reduced from the prior trajectory.

Here are both slides side-by-side, the most recent one on top, the prior quarter’s slide below it.

Micron’s latest outlook slide.

The prior outlook slide.

Micron indicated it will continue to have a hard time with some end markets for its products. For example, in clouddata centers, where server computers need powerful DRAM, the company stated, “Expect cloud demand in 2023 to grow well below historical trend, due to the significant impact of inventory reductions at key customers.”

And for personal computers, the company said in 2023, “PC unit volume to decline by low to mid single digit %.” That is not as bad as the “high teens percentage” decline in 2022.

Absci: Will ‘zero-shot’ AI change drug discovery?

Dec 21, 2022

“We're going to look back on history and realize that that was one of the pivotal moments that changed our industry,” says Absci founder and CEO Sean McClain, “when we put a de novo antibody that was designed on a computer in humans.”

The world was dazzled last month by the debut of an artificial intelligence program called ChatGPT, from the Microsoft-backed startup OpenAI. Posing questions in natural language via the keyboard, a person can prompt GhatGPT to give a full-paragraph answer to a factual question, such as, When did people first land on the moon?

But the same program can spit out endless reams of text, fulfilling much more ambitious queries, such as, Write a poem in the style of Walt Whitman about scuba-diving in Paris.

The wide-open nature of GPT is at the heart of its intrigue. The program seems to have such a broad nature that it prompts one to imagine all sorts of potential applications.

One afternoon this month, at the Manhattan satellite offices of Absci, an eleven-year-old, promising biotech firm, ChatGPT was being put to good use.

“We had a board meeting this week, and I needed something to open up with,” says Sean McClain, founder and CEO of Absci.

“We used ChatGPT to write a rap,” explains McClain, standing amidst the cubicles where the company’s AI team works.

“We asked it, Write a rap on AI drug discovery for biologics.”

“Here we go,” says McClain, nodding to a staffer who starts a beat track on his phone. McClain gives himself a three-count, then launches into the rap with gusto, swaying as he recites each line displayed on the screen in appropriate hip-hop swagger.

AI in the lab, making moves with biologics Fast and precise, our algorithms are prolific Discovering new drugs with efficiency and speed Leaving our competitors in the dust, with no time to bleed

The full poem goes on for several stanzas, as you can see in the accompanying sidebar. The staff gathered around on this Tuesday afternoon are delighted with their boss and give him a round of applause when he’s done.

“ChatGPT wrote that, it’s incredible,” McClain marvels.

He will later inform me, in a follow-up email, that his board of directors, at dinner the next day, upon hearing his rap, “suggested I stick with my day job rather than moonlighting as a rap superstar.”

But that’s alright. The playful diversion is merely meant as an illustration of what McClain believes is being heralded for life sciences by the increasing power of AI programs.

ChatGPT is just one example of a broad class of AI programs known as “generative AI,” applications that don’t just label pictures of cats and dogs, but that instead produce a new artifact in the world.

Today, it is rap lyrics, but down the road, says McClain, generative AI will generate formulas for novel biologics, or drug products, with highly specific powers tuned to the biology of illness.

“The exciting part is being able to be the first company to put a biologic, or an antibody, into humans that was designed on a computer,” says McClain.

“We're going to look back on history and realize that that was one of the pivotal moments that changed our industry, when we put a de novo antibody that was designed on a computer in humans.”

AI’S BROKEN PROMISES

That is a bold statement about drug discovery, and as a journalist, I’m wary. AI in life sciences has been a long time coming, and I’ve heard many claims over the years about its potential. Following McClain’s rap, we sit down in the conference room, and I have a chance to convey my skepticism.

> Write a rap on AI drug discovery for biologics.

OUTPUT:

AI in the lab, making moves with biologics Fast and precise, our algorithms are prolific Discovering new drugs with efficiency and speed Leaving our competitors in the dust, with no time to bleed

(Chorus) AI drug discovery, for biologics Revolutionizing the way we treat our illnesses With precision and power, we're making waves In the world of science, we're the crafters of new days

Our machine learning models are top of the line Finding cures for diseases, one at a time We're changing the game, with our cutting-edge technology Making strides in healthcare, for the betterment of humanity.

(Chorus) AI drug discovery, for biologics Revolutionizing the way we treat our illnesses With precision and power, we're making waves In the world of science, we're the crafters of new days

(Bridge) Gone are the days of trial and error We're using AI to find the right answer Bringing hope to those who need it most With our cutting--edge technology, we're taking the reins and we're on the rise

(Chorus) AI drug discovery, for biologics Revolutionizing the way we treat our illnesses With precision and power, we're making waves In the world of science, we're the crafters of new days

Journalists, including myself, have been like the boy who cried wolf, promising trusting readers about amazing breakthroughs with AI just around the corner.

And yet, to date, no drug has emerged from Phase III clinical trials that can uniquely trace its success to AI. None of the supposed efficiency benefits of AI have changed the economics of the industry.

Instead, the marketplace continues to see upwardly spiraling costs for drugs. Take the recently approved Hemgenix, from the U.S. pharma company CSL Behring of King of Prussia, Pennsylvania. Designed to restore precious clotting proteins to hemophiliacs, Hemgenix is the most expensive drug in the world, at three and a half million dollars per dose, according toNature.

Nor has AI solved the extraordinarily low success rate of drugs that get approved, about four percent of those that are attempted. Even the success rate for Phase I or II trials is stuck at about eighteen percent. For successful drugs, the time frame is still stuck at a decade or more from basic chemistry to Phase III trials.

It feels as if the promise of AI in life science, if not a broken promise, is one that has been extraordinarily over-hyped.

As I recite my chastened view, McClain nods. “I think that we are in the early innings,” he says. “We have shown fundamental advancements in the space, and actually showing, yes, this technology does what they say it can do.”

“That should translate into increased clinical success — but we're not there yet.”

The technology breakthrough to which McClain alludes is encapsulated in a research paper posted by he and his team on the free bioRxiv pre-print server in August. The paper, which has not yet been peer-reviewed, describes how the company used a neural network to predict whether a protein with a certain pattern of amino acids would be more or less likely to “bind” to an antigen — in lay terms, how likely it would be for the protein antibody to attack the pathogen in the body.

Like ChatGPT, the neural network in question is a generative AI program, in this case one introduced in 2019 by scientists at Facebook called RoBERTa, which anyone can grab off the shelf and play with.

The paper showed two remarkable results. One, RoBERTa’s predictions of which antibodies would bind were “highly accurate” compared to what could be measured in the lab by actually observing binding under a microscope. In other words, you could run the experiment on the computer instead of a lot of the lab work, potentially a huge time and materials savings.

More dramatically, McClain and team asked the neural network to invent novel combinations of amino acids by altering sections of known antibodies to create variants. Again, RoBERTa predicted how these new variants would bind and, again, the predictions of the machine were highly accurate compared to what lab results showed.

The point of that second step is that the computer using AI can run many more explorations of possible amino-acid variants than can be run through a lab where the actual assays, even “high-throughput,” take tremendous time and care to prepare.

Similar to how ChatGPT spits out whole stanzas of poetry, the Absci program is able to spit out reams and reams of amino acid variants. In the paper’s results section, McClain and team declared, “Deep language models can expand the search space of an experimental dataset by orders of magnitude.”

As McClain explains it to me, “For drug discovery, it’s essentially saying, Create me a drug that has these attributes — that is the future.” Pharma, he says, then goes “from drug discovery to drug creation, where you’re actually using AI to create novel drugs that don’t exist.”

FROM WET LAB TO AI

It has been a long time coming to this point. McClain founded Absci eleven years ago after graduating a year early from the University of Arizona, where he began as a mechanical engineer but then switched to molecular biology. His focus back then was not on AI, but on the art of protein expression.

McClain’s accomplishment at the start of Absci was a refinement of the mechanism by which E. coli cell lines in the lab can be made to produce enormous volumes of proteins. The cells become like little factories for producing custom proteins that a drug maker would want, such as monoclonal antibodies that can fight viruses.

That was a breakthrough in scale. A typical test tube of animal cells would produce merely thousands of antibodies. With McClain’s approach, “You could basically take a single test-tube of our engineered E. coli, take a billion different antibody sequences, and in that single test-tube you have a billion different drug candidates.”

Absci has patents and patent applications on that protein synthesis with McClain as the lead author. Because it’s rather like a production line for proteins, in an article about Absci for ZDNet earlier this year, I dubbed McClain the Elon Musk of protein manufacturing, a moniker he told me gave him some amusement.

With the ability to mass-produce proteins, McClain’s company was waiting for the proper vehicle to exploit that laboratory capability. The arrival of “deep learning” forms of artificial intelligence appeared on the scene as a perfect complement.

Deep learning is generally data hungry. “There wasn’t enough data” with the mammalian cells of traditional protein research, observes McClain. “We solved that problem.” A billion proteins in a test-tube, rather than thousands, meant there was suddenly enough training data to fit the power of those neural networks such as GPT-3, the generative neural network from OpenAI upon which ChatGPT was built.

“It was basically eleven years at Absci developing the wet lab technology that would allow us to leverage generative AI,” he says.

“The craziest part is, I had no idea that E. coli was going to be the key to unlocking data for biologics with generative AI.”

Shortly before going public in July of last year, Absci bought another startup, Denovium, a three-year-old firm pioneering deep learning AI in medicine. The company was using AI to tease out novel proteins from DNA sequences.

THE FEEDBACK LOOP

Hitched to McClain’s protein factory, the Denovium AI becomes a way to engineer a kind of feedback loop. One first manufactures tons of proteins, then sends the proteins into the AI software, as symbols of amino acid chains, and out come predictions from the program about binding. Those predictions are then sent to the wet lab to be validated in the test tube. The lab validation then becomes further data for the AI programs, and the process starts all over again.

Absci as a company functions a little like a feedback loop. The main headquarters where McClain built his wet lab is in Vancouver, but he flies out once a week or so to New York, where he maintains an apartment, to visit the AI hub on the 43rd floor of 152 West 57th, an imposing modern high-rise next to Carnegie Hall where we are having our chat.

What is discovered in the AI hub in New York becomes the input to the wet lab’s test tubes in Vancouver.

“The fact that we can go from wet lab data, to training the [AI] models, in a six-week time period, that’s what’s allowed us to make these huge advancements in a short amount of time,” says McClain. Other companies have wet labs, such as Recursion Pharmaceuticals, but that is for small-molecule drugs, not large, complex molecules such as antibodies, McClain points out.

The feedback loop has attracted some of the top talent in the field, including AI lead Joshua Meier, who was previously with Facebook’s AI team. Another top AI scientist recently joined from Tesla’s self-driving team.

“They joined because we spent ten years building that feedback loop, and that’s an advantage now no one else has,” McClain tells me.

That tight coupling, says McClain, puts the company ahead of other firms that don’t have a lab, that just use software and data.

“A lot of these papers that are coming out, they say, Hey, we developed this computational metric that got improved,” he says of competing AI efforts. “But they never showed that it worked in the lab.”

The lab is important for ruling out false positives, he says.

"Because we have that six-week cycle time that we have and no one else has, that's what's really allowed us to figure out what directions are important to go in.”

“Sometimes, we see the industry going in a certain direction on a metric that they think is important,” he says, “and we find out that that metric doesn't actually correlate to the wet lab and what we actually want it to do.”

Eventually, says McClain, it will be possible to do most of the work on the computer, in silico, as it’s called. He expects to get there, but it won’t magically happen overnight. It will happen as a progression.

“Ultimately, you're still going to want to validate everything you do” in the lab, he says, "but you're not going to have to validate it to the extent we do now.”

The AI software program developed by Google’s DeepMind program, AlphaFold, is, of course, an important advance in what can be done on the computer. AlphaFold has essentially solved the problem of how proteins fold, the problem of structure, in other words.

Structure is important, but it won’t solve the problem of an antibody binding to an antigen, says McClain.

“Structure is a part of the solution, it’s not the solution,” says McClain. “At the end of the day, you don’t actually care about the structure, you care about, Does the antibody bind to where I want?

“AlphaFold won’t tell me this structure will bind to this target at the affinity I want,” he says. “AlphaFold isn’t telling you how to design the right drug.”

TURNING THE TIDE FOR DRUG DISCOVERY

To my point about the unmet promise of AI, McClain is convinced the feedback loop will dramatically change the success rate in drug development.

“There's never been a technology out there that's been able to, let's say, take a brand new target and be able to design antibodies that hit every single epitope,” meaning, the part on the antigen to which the antibody has to attach. “And, then, to be able to go instantaneously into the lab and say which of these gives me the biology I want to achieve.”

“This is the huge game changer — boom! You can instantaneously know what’s going to give you the biology that you want.”

What’s more, not only binding but also other qualities can be predicted at the same time. In the August paper, the research showed that RoBERTa could predict what Absci has christened “naturalness.” Naturalness means how close is an antibody to naturally occurring antibodies. Greater naturalness can make an antibody easier to produce, and make it more effective against a target in practice.

“You’re not going to have this iterative traditional drug discovery process that takes years and, ultimately, gets sub-optimal hits,” says McClain. “We can get everything right the first time and dramatically reduce the time it takes to get into the clinic.”

By divining both the binding ability of a protein, and its naturalness, “You're no longer having to sacrifice different attributes for each other, and, kind-of, taking suboptimal hits,” says McClain. “You're able to take the optimal hit the first time.”

In AI, the ability of something like ChatGPT to spew out rap lyrics the first time you ask it, without practice, is called “zero shot.” Effectively, McClain is saying that his company’s AI models, in conjunction with the wet lab, will get so good, they’ll be zero shot at generating a good antibody.

“Again, it’s just like how I told ChatGPT to write a rap on drug discovery; we’re going to be able to do that same thing for biologics, feed in the target sequence and have the AI then give us an antibody with all the attributes we want.

“You’re not going to have this iterative traditional drug discovery process that takes years and, ultimately, gets sub-optimal hits,” he says. “We can get everything right the first time and dramatically reduce the time it takes to get into the clinic.”

The normal time to get from chemistry to clinic is four years. “We believe we can get that to about eighteen months,” says McClain.

Following on the success of the paper posted in August, McClain expects that “soon, very soon here, we're going to be releasing where we sit on on the de novo design,” he says, meaning, tailoring a drug from scratch. That may come at an investor conference, he says.

“Things are accelerating faster than we had anticipated,” says McClain.

WORKING WITH BIG PHARMA

Startups don’t generally do their own drug development, and Absci is partnering with multiple drug giants to take its AI and wet lab into the clinic, the most prominent partnership being with Merck.

“Our goal is to be in the clinic in 2024,” says McClain.

To do so, McClain has lured star talent.

A third hub for the company is in Zug, Switzerland, south of Zurich, where pharmaceutical luminary Andreas Busch runs the company’s “innovation center.”

Busch had been on the board for four months when McClain said, “We need you full time” to oversee the company’s work with the drug makers.

Busch has the important duty of bringing traditional Swiss cookie samplings with him on his trips to the New York office, which he puts out in the common area for all to enjoy. He finds New York fascinating, he tells me, but confesses the pace and complexity make him happy to return to the sleepy terrain of Zug.

He also has the important duty of being a steady hand who’s seen the full cycle of drug development. The sleepy Zug canton is, in fact, the locale of many Big Pharma companies, and Busch has helped to run R&D at many of them, including Sanofi, Bayer, and Shire.

“It’s incredible that we even landed Andreas,” says McClain. “He is one of the most prolific R&D, large pharma executives in the industry, I mean, he’s gotten over ten drugs approved, all the way from the bench, which, I think, is more than any other large pharma exec.”

McClain with chief innovation officer Andreas Busch, center, and chief AI officer Joshua Meier, in the company’s New York satellite office. The unique assets such as the wet lab have been a big factor in attracting “the best of the best” in talent, says McClain.

EXPLAINING THE ODDS TO INVESTORS

All of this research has to come to market, and what expectations to set with investors is a complex matter. Absci is growing very fast off of a very small base of revenue. The Street models sales doubling to a little over nine million dollars this year, and almost doubling again next year to eighteen million.

Absci releases quarterly press releases, but it has not held the traditional conference call with Street analysts since coming public. The stock is covered by a handful of analysts including Credit Suisse, Cowen & Co., and Stifel Nicolaus.

“We didn’t want to set a precedent of doing it [conference calls] because we’re not an earnings story,” says McClain.

All investors, including Fidelity Investments, the second-largest holder, says McClain, know that “It’s going to take time for revenue to ramp up.” In the breach, the right metric to watch is the company’s programs with Big Pharma. Those programs pay out in multiple ways, starting with up-front payments, followed by payments for milestones achieved, followed by, someday, royalties, assuming a drug succeeds.

So far this year, Absci is ahead of its intended goal of signing eight programs with pharma companies, having achieved ten, including three with Merck. The Merck deals, which carry the option of collaborating on three different drug targets, are valued at $610 million in milestone payments and eventual royalties. Meaning, up-front payments and milestone payments to Absci would be about $200 million per drug.

“Building up that portfolio [of programs], things get more advanced, and that's when you start getting that cascade of large milestone payments being hit, and ultimately, ramp up to royalties,” explains McClain.

The company doesn’t say how much the up-front payments are that are baked into each deal. “I will say it is a significant payment that definitely covers the cost of the work that will be done.” Revenue of $2.4 million in the most recent quarter was mostly from milestone payments by Merck, the company has said.

Given that it can take time for the total $610 million value of something like the Merck deals to be realized — if ever — Absci’s CFO, Greg Schiffman, will point out at investor meetings that the net present value, the discounted cash flows, of future deals is in the neighborhood of $15 million to $20 million per program.

“The way to think about it is, if we were today to go to a royalty farm that buys royalty streams, they would pay you today $15 million to $20 million for that particular program,” says McClain. “And so, if you did ten programs, that’s $150 million to $200 million of lifetime value that you’ve created; you’re not recognizing it today, but if you wanted to, you could go off and sell those.”

McClain is quick to add “But that’s not the business model,” meaning, selling the royalties.

As far as the ramp, while it’s highly dependent on what happens in the lab, and the AI hub, and the clinical path, it’s also tied to clinical success and commercial marketing if a drug happens to make it that far.

“You could think of it as, a good chunk of it is in-clinical development, and then we get royalties on top of that,” says McClain. “I would expect in the next three to five years, we will see revenues ramping up significantly, and really starting to create that hockey stick from a revenue perspective.”

Those milestones can come quicker if Absci can boost those dismal success rates of four percent overall and eighteen percent for Phase I and II trials. The bet McClain and team are making is that they improve those success rates, which would improve the payoff represented by net present value.

“All of our investors and analysts know that that's highly conservative,” he says of the $15 million to $20 million estimates. “Because with our technology, it should — and it will — in future increase success rates,” he says. “Even if you go from four percent to eight percent” success rate for drugs, he says, “that’s huge, even just on a net present value basis, that’s going from $15 million or $20 million to $30 million to $40 million — you double success, you double the NPV.”

PROOF OF CONCEPT

At the same time that it partners with Merck, says McClain, Absci will pursue some programs of its own. “We’re actually going to be developing our own pipeline” of drugs he says. “We don’t plan on taking these to Phase III, because that’s extremely expensive, but if you can take it to a proof of concept, let’s say, get an efficacy readout in Phase I, that’s a huge value to the asset.”

He predicts “we’re going to be able to get there faster than anybody else can,” meaning, getting to a Phase I. As for what those drugs might be, it won’t be a cure for cancer, he says. Rather, the orphan drug market, where disease cohorts are small enough that they usually don’t attract much investment, “is a really interesting area,” he says. He declines to say which indications those might be, but says the company intends to disclose that next year.

Getting to a Phase I trials with its own drug, and proving the Absci feedback loop, “gives you huge credibility, huge validation that the platform works, and that’s going to be driving even more partnerships our way,” observes McClain.

While oncology is off the table for the moment, McClain does allow as the topic is an intriguing one.

“The issue with oncology is that everyone’s going after the same known targets,” he says. “What we need to do is actually find new targets.”

PATENTS PENDING

If the company finds new targets for anything, it opens up a whole other aspect of the business: patents. The more that drug discovery turns to drug design, the more that Absci may be able to establish patents on both antibodies and drug targets, says McClain.

“We have very broad IP here,” says McClain. That includes both the wet lab technology of protein expression and whatever is developed with AI.

“If you can take a novel target, use the platform to develop antibodies against all the epitopes [locations on the target], then that enables you to make patent claims that you couldn’t have enabled in any other way.”

The dynamic of designing antibodies and linking them to the antigen becomes a kind of circular dynamic that establishes exclusivity, says McClain.

“You give yourself a big runway to go after that target where no one else could come in after you because you’ve defined the target as a function of the sequence variety [of the antibody] that goes after it.”

The company’s general counsel, Sarah Korman, who had been the head of IP and licensing at Amgen, was lured to Absci in part because of the patent prospects, McClain tells me.

“She saw the diversity that our AI models could create, and how that could actually enable very broad patent claims that previously were unattainable,” says McClain.

“Broad claims means you can block other people, and ultimately, kind-of, dictate who can come into a target.”

A power, no doubt, one must wield carefully, I offer.

“No, absolutely,” replies McClain. “You have to always remain, What is best for patients? How do we do what’s best for patients, and make money, and create shareholder value?”

THE BEGINNING OF THE ROAD?

If, as he says, Absci gets into the clinic in 2024, and if its AI models are really “zero shot” drug development machines, how soon will it be clear that this whole approach is going to make good on the promise of AI? Is it ten years down the road? Is it more than that?

“No, I think you’re going to see clinical proof of concept way sooner than ten years,” says McClain. “Even being able to get a Phase I efficacy readout, so you can actually show something that gets people excited, and then you go to Phase II and show that proof of concept.”

“This goes back to having somebody like Andreas on board that really knows the clinical development side, knows where to look for targets that could give us early efficacy signals in a phase one.”

It is still early innings, McClain reminds me again, as we wrap up. “I think the public needs to know that,” he says. “But, early innings are exciting.”

I’m reminded of cancer biologist Robert A. Weinberg’s great book, Racing to the Beginning of the Road. Weinberg wrote that the 1970s and 1980s were the decades that taught scientists the mechanism of cancer, why cells go rogue, why programmed cell death fails to rein in chaos.

Looking back from the 1990s on those decades of fitful, meandering research, Weinberg declared, hopefully, “after so long, we finally know where to look” for a cure.

Perhaps after years of work in wet labs and in AI, McClain and others have the tools they need to begin to make serious breakthroughs.

As we walk to the elevators, McClain, Absci’s single largest individual shareholder, with just under ten percent of the stock, tells me, “I think this will show you my bullishness: in eleven years, I haven’t sold a single share of stock.”

Absci shares, at a recent $2.38, are down seventy-one percent this year, and down eighty percent since IPO.

Nvidia: buy it, it’s troughed, says Needham

Dec 20, 2022

After a forty-four percent decline in shares of Nvidia this year, expectations for the chip giant have been thoroughly washed out, and now is the time to buy the stock, writes Needham & Co. analyst Rajvindra Gill in a note to clients Monday.

“NVIDIA is our Top Pick for 2023, and we are adding it to the Needham Conviction List,” writes Gill, while raising his price target on the shares to $230 from $200, and reiterating a Buy rating.

Estimates for Nvidia, notes Gill, have been cut by fourteen percent this year for the company’s revenue in 2022, from $31.2 billion to $26.9 billion, and the earnings per share estimate has been cut by thirty-four percent. (Nvidia’s fiscal year actually ends in January, but Gill uses calendar years to simplify the matter.)

For 2023, estimates have been slashed by twenty percent for revenue and thirty-one percent for EPS.

Gill argues that the company’s slump in sales of video game cards is about to come to an end, writing “Gaming revenue has bottomed (inventory cleared exiting this year).”

You’ll recall that Nvidia cut its expectations in August because of rising inventory of GPU chips brought on by slowing sales in the video game market.

Following that, CEO Jensen Huang told the Street last month that Nvidia is finally finding its footing in the gaming market. “We are quickly adapting to the macro environment, correcting inventory levels and paving the way for new products,” he said at the time.

Meantime, writes Gill, the data center market, which is actually the larger category of product for Nvidia “remains on a solid footing,” excluding the weakening of sales into China’s data centers.

The data center market, moreover, is extra attractive given that Nvidia is dominating sales of “GPU-based accelerator cards” that speed up server tasks. Citing data from Gartner, Gill writes that such cards have an “attach rate” of sixteen percent, meaning, sixteen percent of servers sold sell with one of those cards. “We believe NVDA dominates the market here; corroborated by our Top500 analysis” of supercomputers, he writes. That dominance, he argues, is prompting customers to upgrade to Nvidia’s latest and greatest GPU for data centers, the “H100,” or “Hopper” chip that came out this fall.

See also:

Nvidia CEO Huang: cloud expands the company’s reach into enterprises, November 15th;

Nvidia’s forecast in-line with street, says ‘quickly adapting’ to global economic slowdown, November 15th.

Last, the valuation has come down for Nvidia, even if it’s still pricey. The multiple of enterprise value to sales for calendar 2022 estimated sales is 15.4 times, which is down thirty-five percent from what it was at the beginning of the year. And the multiple for next year’s estimated sales is 14.3 times, down twenty-nine percent.

“Nvidia’s multiples have come down significantly since the start of the year, alongside its stock price,” writes Gill.

That means Nvidia’s stock is less risky than the broader market, he opines:

Market multiples have expanded meaningfully since the October bottom. We posed the question “is this the bottom another head fake?” in our recent earnings review. We expect the first half of CY23 to remain choppy as estimates likely need to come down further. Yet for NVDA, we think estimates are much closer to the bottom. We believe the shares can trade closer to their pre-COVID levels as both Gaming and Data Center growth accelerates in 2H23.

Nvidia shares, despite Gill’s positive missive, closed down two percent Monday.

Nvidia is one of the TL20 stocks to consider. Its shares are up three percent since the TL20 was inaugurated in July.

The TL podcast for December 18th, 2022: Chip stocks break their winning streak, and what ails Tesla

Dec 19, 2022

News of the Fed Reserve half-a-point hike on Wednesday sent everything into sharp decline, but chips stocks, in particular, have reversed their recent winning streak. Tesla (TSLA) was one of the biggest losers of the week, and Elon Musk could fix what ails the stock if he’d make more disclosure about metrics around car sales.

Tesla: Musk needs to give some Metrics

Dec 18, 2022

A week ago or so, I received a tweet in my Twitter feed from Elon Musk, informing me that Twitter’s average load time has improved by four hundred milliseconds. I doubt I noticed the difference, and I doubt many other Twitter users did either.

Frankly, while Musk is re-arranging the deck chairs at Twitter, I suspect most investors would be a lot more interested to hear more from him about measurement at the one company of his that has the most prospect of actually being a great business, Tesla.

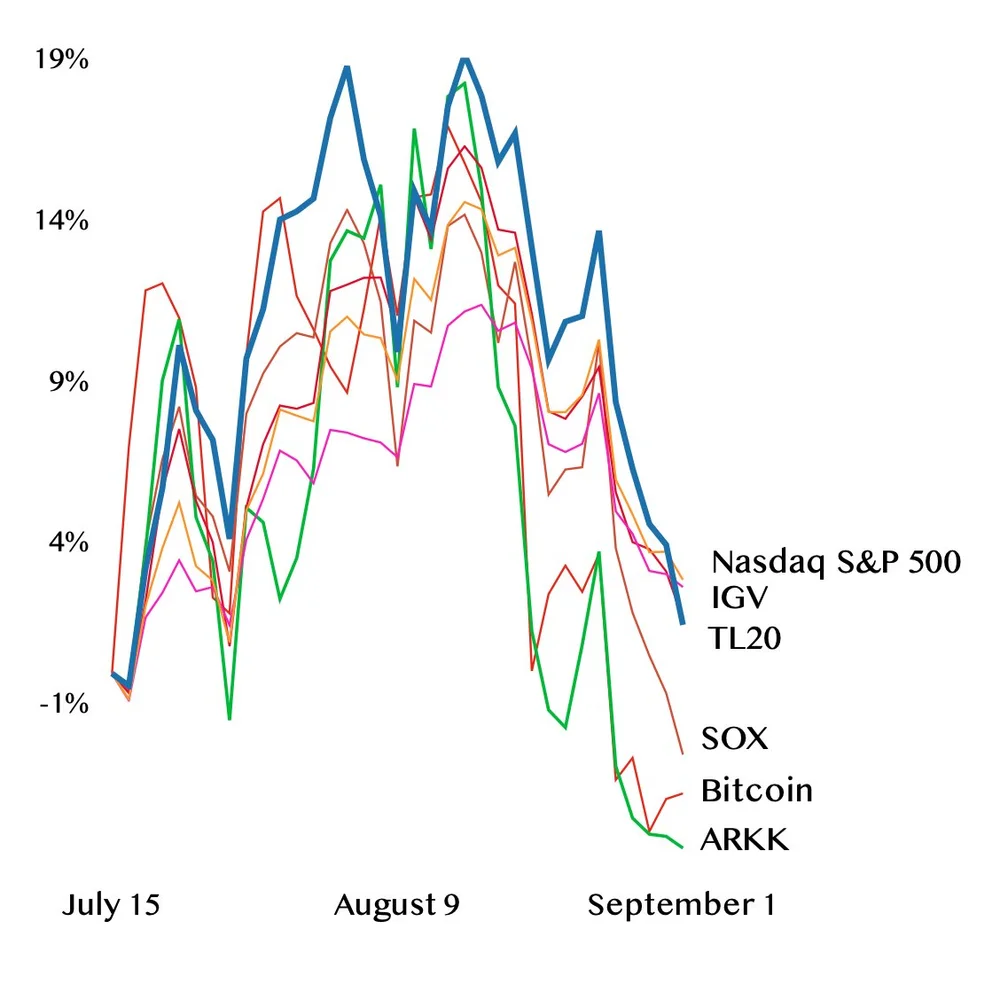

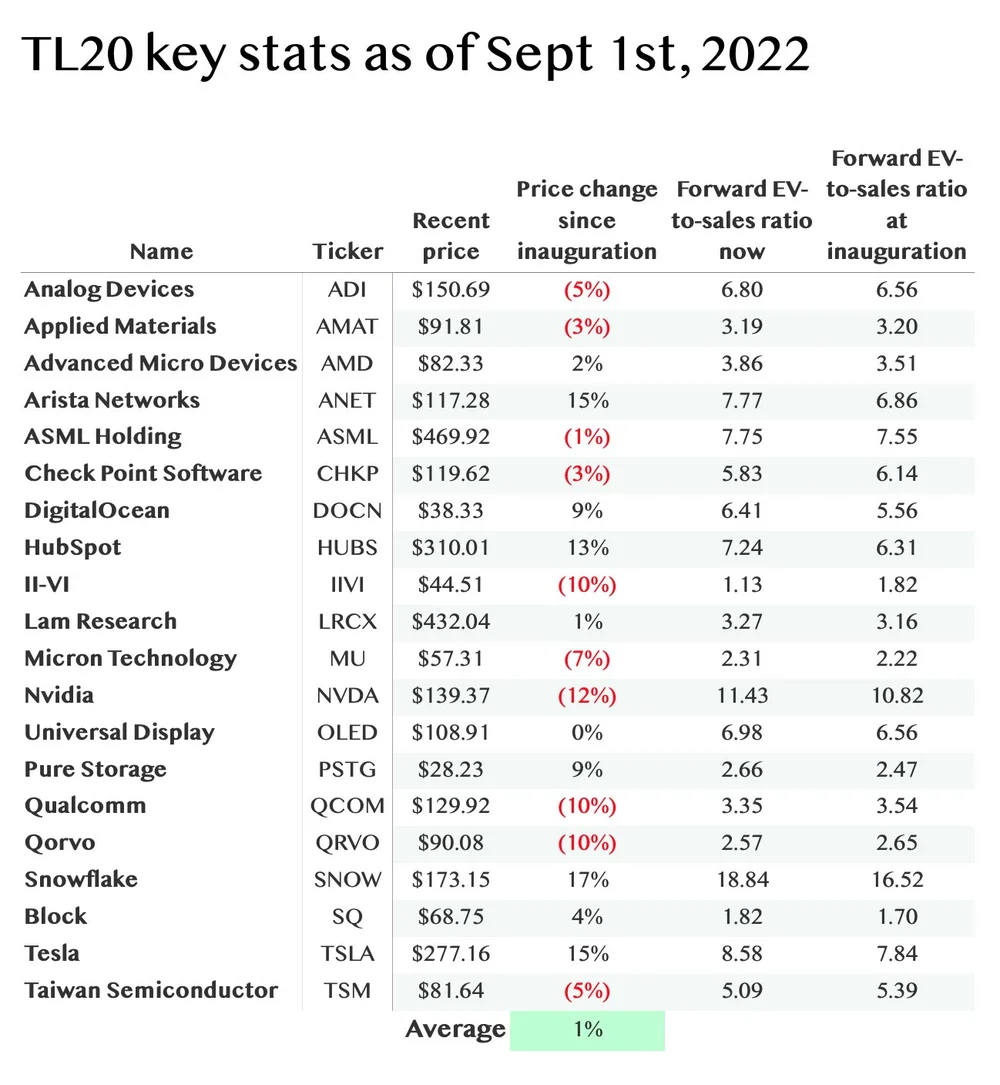

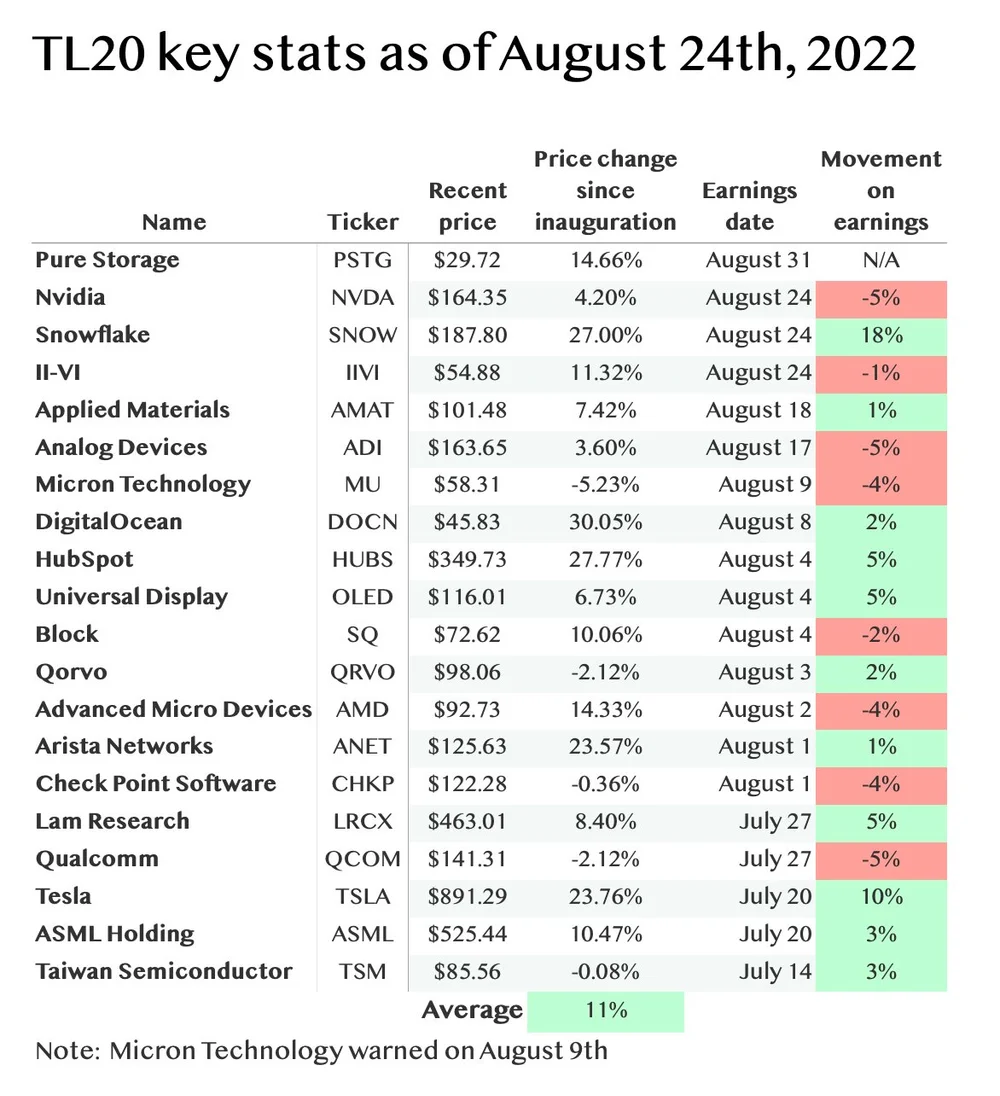

Tesla has been a real dog for the past four months or so. I refer to that amount of time because it is the time since inception of TL20, The Technology Letter Twenty, the list of twenty great companies to consider investing in. Tesla is a great company, and it’s one of the TL20. It could be a great stock, but it’s been terrible since the inauguration of The Twenty.

Tesla is the worst performer since the July 15th inauguration date, down thirty-seven percent. Because the TL20 is market cap-weighted, Tesla exercises a substantial effect upon the group. The entire TL20 is down 12.6% since inception, but excluding Tesla, it would be down just 2.2%.

By that alternate measure, the TL20 would be ahead of the 6.5% decline in The Nasdaq Composite Index since July 15th, and it would be a lot closer to the Standard & Poor’s 500 Index, which is roughly flat since July.

What will stem this decline? What might help is if Musk were to share more data about how Tesla’s sales prospects look. The data the company traditionally discloses is vague, and has lately become very cloudy and hard to interpret.

That is happening at a time when there is rising anxiety that Tesla’s sales may be about to fall apart. Tesla is a bubble stock, and to an extent, a bubble company, and it has never been tested in a prolonged economic downturn.

Founded in 2003, Tesla came public June 28th of 2010, after the last major economic contraction, The Great Recession. Its vehicles, which list starting at just under fifty thousand dollars for the base Model 3, represent pricing in a time of relative economic prosperity.

In an economic crunch, even some bulls think Tesla will have to cut prices. An Uber-bull on the stock, Trip Chowdhry of the boutique Global Equities Research, writes in recent missives to investors that both Tesla, and competitor Lucid Group, “will need to drop vehicle prices by at least 10% to 15%” because neither is “immune to recession.”

If it is true that Tesla is now entering its first real test of demand, it might be good to have a more solid measure of demand. That’s where metrics come in.

Tesla’s financial reporting has to date consisted of a two-step: deliveries and revenue. Tesla recognizes revenue on cars only when the customer takes possession of the vehicle, the delivery. The company reports total car deliveries shortly after a quarter is over, and two weeks later, it reports revenue. In between, the Street writes predictions about revenue using deliveries as a leading indicator.

That kind of very simple calculus is a thing that works just fine when business is going up and up in good times, much as Netflix, another bubble company, for a long time dazzled the Street with rising subscriber numbers — until it stopped growing.

For Tesla, deliveries have become problematic as a reflection of anything of late because they’re under pressure from factors unrelated to demand.

Tesla, like many firms that make real, physical stuff, has been dealing with the supply chain issue. As a result, deliveries lately are not keeping up with expectations. Musk, and CFO Zachary Kirkhorn, have set a goal to increase both production of cars and deliveries, on a unit basis, by fifty percent, annually, over a multi-year time horizon. Production rose fifty-four percent last quarter, but deliveries rose only forty-two percent, and Musk and Kirkhorn said deliveries will continue to be under pressure.

The Street expects deliveries will still be under pressure in 2023, forecasting total delivery growth of just forty-four percent next year.

There’s a second reason deliveries are cloudy, and that’s the rising backlog of cars not delivered. The company has been raising prices this year to offset rising costs, not just materials costs but the rising cost of freight.

Consequently, cars in backlog, once they are delivered and recognized as revenue, will probably skew Tesla’s average pricing upward irrespective of demand. That can cloud Tesla’s true pricing power, quarter to quarter.

If deliveries aren’t a great indicator of demand, Tesla’s actual commentary about demand is vague.

Musk and Kirkhorn typically talk about how the “order book” is doing in broad terms. On the October earnings call, Musk remarked that, “demand is a little higher than it would otherwise be,” without elaborating.

It would be nice to have another measure of demand. The balance sheet provides some extra data, but not much. The deferred revenue balance includes many parts of Tesla’s offering that have nothing do with the vehicle sale itself, such as the company’s self-driving software and system software updates.

The other balance sheet metric that’s slightly relevant is the figure of Tesla’s customer deposits, which is the amount a customer has to put down when they place an order, such as the $250 deposit for a base Model 3. But that figure also includes deposits for Tesla energy products, so it’s not a clean auto number.

And the deposit amount per vehicle is highly variable based on the model and configurations. To my knowledge, no one has triangulated how customer deposits correlate to aggregate car demand for Tesla in any given period.

So, there is no good measure for demand, other than Musk’s upbeat tone — that, and the company’s past performance of generally increasing sales nicely over many years.

Other areas of tech have come up with additional measures to reassure investors. The prime example is the software industry.

A year ago, I wrote a broad overview about how the software world has sprouted numerous measures of the business quarter to quarter. The Metrics, as I term them, include tons of non-GAAP numbers such as “remaining performance obligation,” a measure of the total value of software contracts signed that has yet to be realized as revenue.

If Musk and Kirkhorn had any desire to reassure the investing public, they could disclose a similar sort of measure. For example, what is the total order book value in dollar terms? How much of that might be realized in a given period, the current portion of the order book, would be a nice complement.

Based on the remarks and tone of the conference calls, I don’t get the sense Musk and Kirkhorn have any urgency to provide such reassurance. And I expect they don’t want competitors to know those kinds of things.

That means investors will have to decide: Is this a company that’s priced too high for a recession, or will its position as an EV leader prove more durable than people suspect?

Even in a tough market, if prices fall as Chowdhry expects, Tesla would still be the best house in a bad neighborhood, as it is far ahead of the competition in making product.

I wrote last month that the crop of young contenders are a mess. Lucid, Rivian Automotive and Faraday Future have continued to miss expectations as they struggle to get to volume production. All three, moreover, are pricing their wares at the high end of the market, so none of them are a budget alternative.

Ford and others can be a budget alternative, buttheir progress in EV sales still leave them far behind Tesla. A report in November by S&P Global Mobility stated that of 525,000 electric vehicles registered in the U.S. in the first nine months of this year, sixty-five percent, 340,000, were Teslas.

Ford has sold a total of 53,752 electric vehicles this year, making it number two behind Tesla, according toThe Detroit News’s Jordyn Grzelewski. While Tesla doesn’t report regional numbers, you could say that based on deliveries of 343,830 cars, worldwide, in the third quarter alone, there is good reason to believe Ford is a very distant second place.

If Tesla isn’t recession resistant, but if management won’t reassure investors with additional disclosure, then at some point, the prospect of share buybacks will probably become one of the most important parts of the story.